Have to be in it to win it. Should I buy or sell?

Trying to time the market rarely works in the long-run

Short-term volatility may induce investors to deviate away from their core investment philosophy of a long-term buy-and-hold strategy in an attempt to chase higher returns. The opportunity of trying to time the market may seem clear and enticing in retrospect but is rarely visible in prospect. Empirical evidence suggests that market timing strategies have a minimal success rate, and over time, this success rate becomes minuscule.

Continuously aiming to generate alpha (excess return compared to its expected return) by buying low and selling high requires more frequent trading and, in turn, increases the trading costs for a portfolio, which are ultimately passed onto you, the investor. Numerous studies have provided empirical evidence to support that buy-and-hold strategies deliver superior annualised returns compared to market timing strategies.

A study by Putnam Investments shows that $10,000 invested in the S&P 500 using a buy-and-hold strategy between 31st December 2006 and 31st December 2021 would have given investors an annualised return of 10.66%—5.61% higher than those investors who missed the best 10 days during that same period. [1]

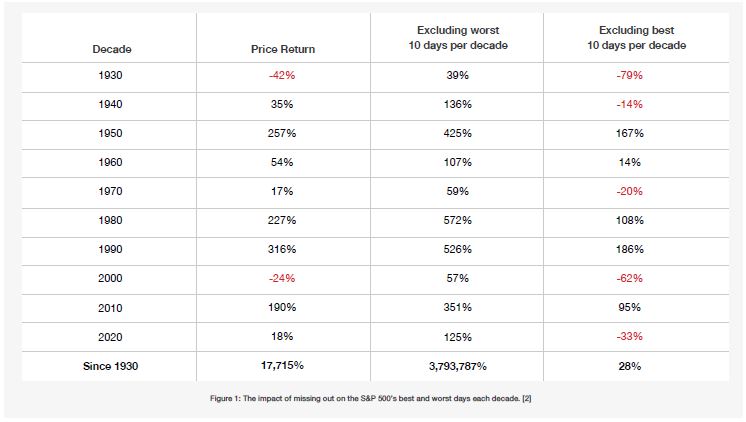

Data from the Bank of America shows that a buy-and-hold strategy invested into the S&P 500 since 1930 would have produced 17,715%, compared to just 28% if an investor had missed out on the best 10 days per decade.

During different economic cycles, some investors collectively develop a herd instinct, replicating the investment strategies of others. This is especially evident during volatile and bearish periods, when some investors panic and sell due to fears of plummeting prices and continuous negative returns.

As a result, behavioural biases take over investment philosophy and strategy. Panic selling can significantly lower cumulative investment growth for long-term investors, as it causes them to miss out on the best-performing days.

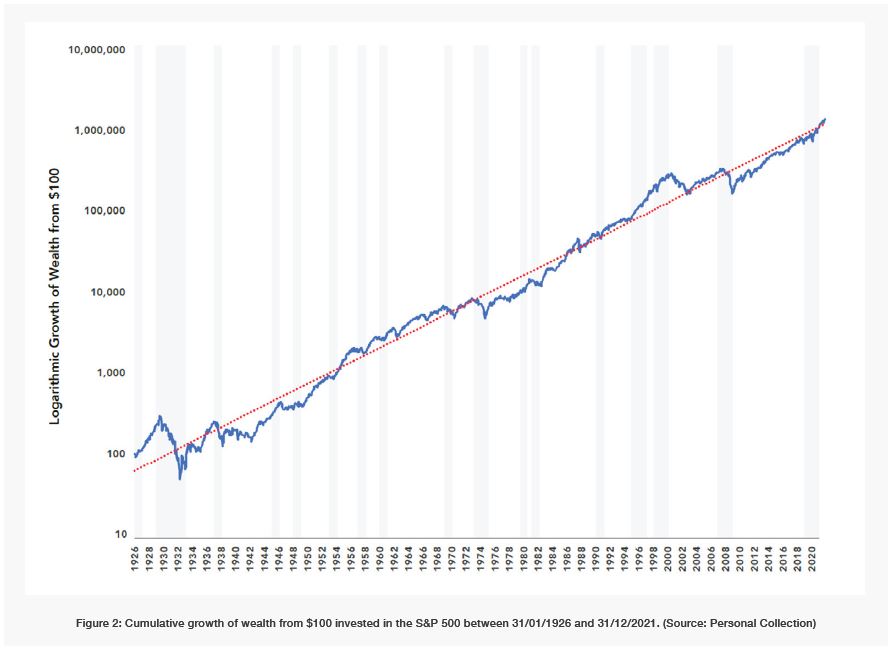

Figure 2 illustrates the cumulative growth that an investor could have derived from $100 over the last century, irrespective of the highlighted recessionary periods.

Past performance is not necessarily indicative of future results.

Behavioural Biases Take Over

A typical economic cycle lasts 5–6 years, though this varies depending on numerous factors, including monetary and fiscal policies set by the government in that market.

The descriptions below illustrates the standard economic cycle, showing how the economy moves from boom to bust and back to boom. Alongside this, it highlights behavioural economics, explaining why people behave the way they do in the real world.

Economic Cycle & Investor Behaviour

Bottom

At a market bottom, investors are demoralised and pessimistic. All good news is viewed as bad news, and while company fundamentals are improving, they are largely ignored. At times like this, the only part of the company’s financial statements that anyone looks at is the balance sheet. Investors want to know that the company isn’t about to go out of business.

The worst part of being in this stage is that it is a fool who tries to call a bottom (or top), so we never know when the gloom will end. Everything is bleak, and investors yearn for better days.

Early Stage Recovery

Companies see their operational fundamentals improving, and so many of these companies have been beaten up that bargains abound for value investors.

Sadly, though, these investors are still jittery from the recent bloodletting, and no one is keen to be first back in the water. Gradually, however, valuations become so compelling due to better fundamentals, investors begin dipping their toes in again. There is hope for investors and a light at the end of the tunnel.

Mid-stage Bull Market

There is positive market sentiment and excitement. Let the good times roll!

Companies are emerging from their slumber, consumers are filled with confidence, and optimism hangs in the air like a sweet summer breeze. Investors are buoyed by improving numbers, but also equally importantly by a newfound optimism. They are once again willing to pay up for stocks, particularly those with strong growth.

Late-stage (and peak) Bull Market

This is the stage where investors begin to buy into excessively optimistic projections, and the market bottom is so far in the rear-view mirror that we can no longer make it out.

The fear now is not of falling prices; the fear is of missing out on the bonanza. Euphoria and greed are the order of the day. Models are upwardly revised, and doubts are ameliorated.

Bear Market

Like a Sunday morning hangover, when a bear market unfurls, we begin to realise that our ‘investment goggles’ made that stock appear a whole lot more attractive than it actually was.

Our awareness that conditions and fundamentals are deteriorating is brought into sharper focus, and we begin to realise that we have vastly overvalued the market. We feel all at sea and start to seek out a safe harbor.

Continuous Buying and Selling Increases Overall Costs

Behavioural biases influenced by changes in the economic cycle can lead investors and portfolio managers to adjust their investment strategies. While a more active approach may offer the potential for added returns, it also comes with increased risks and costs.

Different strategies require frequent changes in asset and security allocations, leading to higher trading and transaction costs. Over time, these costs can significantly drag down investment performance. While they may seem insignificant at first, they accumulate and compound along with investment returns.

Continuously changing asset allocations can also increase portfolio turnover rates, resulting in even higher turnover costs.

What Should Investors Do?

We believe longer-term investors should maintain discipline and self-control, staying committed to their original plan rather than reacting to short-term market turbulence.

Unless your financial goals or circumstances have changed, there is no need to alter the investment portfolio. It’s crucial to remember that consumption has not stopped permanently—it has only been temporarily paused. When markets react to bad news, investors should remain focused on the long term and avoid impulsive decisions.

The best approach is to diversify across regions and asset classes while exercising patience. As long-term investors, we do not attempt to time the market. Instead, we believe that staying invested will ultimately lead to success.

References

[1] 2022. Time, not timing, is the best way to capitalize on stock market gains. Putnam Investments.

[2] Stevens, P., 2021. This chart shows why investors should never try to time the stock market. CNBC.com

Disclaimer

We do not accept any liability for any loss or damage incurred as a result of acting or not acting based on the information in our publications. You acknowledge that you use this information at your own risk.

Our publications do not constitute investment advice, and nothing within them should be construed as such. They are intended to provide information and education for clients to discuss with their financial advisers who have the relevant expertise to make help and advise on investment decisions.

The information we publish has been obtained from, or is based on, sources we believe to be accurate and complete. Where the information includes pricing or performance data, it has been sourced from company reports, financial reporting services, periodicals, and other reliable sources. While we take reasonable care, we cannot guarantee the accuracy or completeness of any published information. Any opinions expressed may be incorrect and are subject to change at any time. Investors should always conduct their own independent verification of facts and data before making investment decisions.

The value of shares and investments—as well as the income derived from them—can fluctuate, and investors may not get back the amount originally invested. Past performance is not necessarily indicative of future results.